Telco/ICT Sector Can Change the Sustainability Game

The ICT sector is now responsible for 3% to 4% of global CO2 emissions, about twice the level of the much more heavily scrutinized aviation sector. Given that global data use was estimated to grow 60% in 2021 alone, the industry could be responsible for up to 14% of global CO2 emissions by 2040. That is unless significant steps are taken to lower the environmental impact of telco and communication technology companies.

Within the ICT sector, telcos are responsible for 1.6% of total global CO2 emissions. Up to 90% of emissions from telco companies come from upstream and downstream activities, such as the energy consumption of their suppliers.

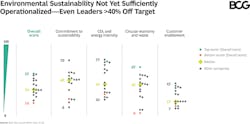

In the past, telco CEOs have been reluctant to make sustainability a top strategic priority, seeing it as a cost topic best left to internal sustainability departments. But in fact, sustainability is a strategic topic with substantial potential returns in terms of savings and new product offerings that CEOs need to own. To gain insight into these issues, BCG launched its Telco Sustainability Index, which zeroes in on how to measure sustainability and what steps are necessary to implement a sustainability approach for the entire business. (See Figure 1.)

As a specific segment within the ICT industry, telco operators have a sizeable impact on both CO2 emissions and waste. To assess the CO2 impact, companies need to consider all 3 scopes of emissions.

- Scope 1 emissions: Telcos generate few of these as they don’t directly burn fossil fuels.

- Scope 2 emissions result from purchasing energy and heat. This infers what is in scope 2 for a telco is in scope 1 for the energy supplier as a vendor of the telco.

- Scope 3 emissions are caused by downstream and upstream activities, such as the energy consumption of suppliers. This is by far the biggest impact area, typically making up more than two-thirds of a telco’s total carbon emissions, and sometimes more than 90%. In the past few years, most telcos have begun to acknowledge that they should assume responsibility for their scope 3 emissions, for example by demanding transparency into their suppliers’ footprints, engaging with them to improve, and factoring this into the selection process.

In addition to lowering their own end-to-end emissions, telcos have a historic opportunity to help other industries become more energy efficient. Smart products and solutions from telcos (e.g., smart agriculture and smart logistics) are already available that can help other industries reduce their carbon emissions by an amount up to 10 times the telco industry’s own emissions. This customer enablement is becoming a key measure of a telco’s environmental performance and a major avenue for boosting its B2B business.

Besides energy efficiency, telcos could help companies save energy by replacing high carbon physical products and activities with virtual low carbon equivalents (a.k.a. dematerialization).

Also, telcos with IT activities could play a big role in helping companies use so-called digital twins to simulate the performance of physical assets, processes, people, places, systems, and devices. For example, a company could create a digital simulation of an aircraft engine and feed in data so that the simulation behaves like the real thing. This way a company can learn how the engine performs in various circumstances, and also discover opportunities for reducing emission intensity.

The Green Bottom Line

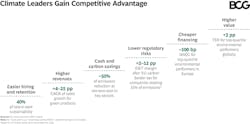

For companies willing to think broadly about how to advance their sustainability initiatives, technology can act as a major accelerant. We call this mindset technology eco-advantage—using advanced technologies and ways of working to enable profitable solutions that also have a positive impact on net zero and other environmental, social, and governance goals.Climate leaders can attract and retain better talent, realize higher growth, save costs, avoid regulatory risk, access cheaper capital, and achieve higher shareholder returns. (See Figure 2.)

Up to this point in time, the telco sector hasn’t been subjected to the same level of scrutiny and criticism as other high-emitting sectors of the economy. We believe that situation will quickly change. Those telcos that anticipate this shift and put in place meaningful and actionable strategies will reduce their environmental impacts, save costs, and win customers.

Thankfully, the ICT/Telco industry is increasingly serious about reducing its direct and indirect carbon footprint, the BCG report notes. Most major telcos have signed up to reduce the energy needed per unit of traffic by about 70% by the end of this decade. BCG estimates that action by the ICT industry could eliminate up to 15% of all global emissions by 2030, more than a third of the total emissions reductions needed to meet global sustainability targets. In total, 12.1 gigatons of CO2 could be saved, which equates to $6.5 trillion.